Maximize Value When Selling Your Business – Get Rid Of Excess Inventory

When selling a business, maximizing value is of primary importance to the business owner. One element that can drag down business value is poor inventory management in the form of excess inventory. Maintaining proper inventory levels is essential to maximizing value.

When running a business, the goal should be to tie up as little cash as possible in inventory, while having enough inventory to meet ordinary business needs. After all, a prospective buyer looking at your business as a possible acquisition would rather have fully flexible cash not less flexible inventory weighing profits down. Any additional dollar that can be found to help bottom line earnings when selling a business will be rewarded by a higher price when the business is sold.

There is a delicate balance where it begins to cost more to carry the inventory than it costs to not carry the inventory. Carrying unneeded inventory can decimate profitability and cash flow in a hurry. Not only does excess inventory tie up a lot of cash, but there are day-in and day-out costs associated with that inventory as well. From the expense of financing that inventory, to the costs of markdowns due to age and obsolescence, to the incremental payroll costs of moving it around, to the hidden costs of not being able to merchandise more productive inventory in its place, it all adds up, and hits the bottom line.

These costs affect the profitability of the business and include, but are not limited to, the following:

- Cost of Capital – There is a cost of the capital that you have tied up in inventory which may be in the form of interest that you are paying for the financing of the inventory. With every sales transaction, cash is generated, which drives the operating cycle. Cash is used to purchase inventory and pay expenses. But when your inventory is too high, your cash is tied up in that inventory. In cases where inventory is not being converted to cash efficiently, the need for an increased line of credit is the consequence. Paying more interest on the increased debt is obviously costly when you should be generating those funds internally.

- Storage – There is a cost for taking up space in a warehouse. You may be leasing more space than you actually need. You may also have higher utility expenses that are associated with leasing this larger space.

- Handling – There is a cost associated with servicing and maintaining inventory such as material handlers and recordkeeping staff.

- Opportunity Costs – This cost is associated with the funds you have tied up that you cannot put to use elsewhere. This cost can be determined by evaluating what you could have done with the money if you hadn’t spent it on inventory. Whether it is investing in upgraded technology, equipment, staff, or something else you could have done with that money. Any higher gains that could have been achieved from those other investments is a lost opportunity and is a cost of carrying inventory.

- Insurance and Taxes – You may be paying more taxes and higher insurance premiums than necessary to maintain excess inventory.

- Risk of obsolescence – There is an increased chance for obsolesce, deterioration, or damage when you have too much inventory.

- Higher Selling and Advertising Costs – If you are carrying an excess level of inventory, you will incur additional and probably unplanned selling and advertising expenses in order to sell the excess merchandise.

There are other issues concerning inventory that can derail the successful sale of a business. Be sure to discuss any inventory issues you may have with your business broker prior to marketing the business for sale.

Read More

IBBA and M&A Source Market Pulse Survey Report Predicts Major Changes

The IBBA and M&A Source Market Pulse Survey Report for the fourth quarter of 2018 has a range of interesting insights. The survey’s purpose is to provide an “accurate understanding of market conditions for businesses being sold in Main Street (values $0-$2MM) and the Lower Middle Market (values $2MM-$50MM). This national survey was designed as a tool for business owners and their advisors and has the support of both the Pepperdine Private Capital Markets Projects and the Pepperdine Graziadio Business School.

One of the most striking facts to leap out of the report is the fact that a full one-third of advisors fully expect the strong market to end this year. Overall, advisors are not optimistic that the current climate will continue through 2020. In fact, advisors are encouraging sellers to consider placing their businesses on the market now, while the market is still strong. This is according to Craig Everett, PhD and Assistant Professor of Finance and Director of the Pepperdine Private Capital Markets Project.

One fact from the report that could be overlooked is that only a mere 8% of advisors expect the current climate to last for 48 months or more. Additionally, only 9% believe that the current climate will last between 24 to 48 months. Perhaps most striking of all is the fact that 60% of advisors feel that the current climate will end within the next two years.

Business owners who are considering selling should be advised that almost two-thirds of advisors now feel that there will be a significant shift in the next two years. Considering that it can take a year or more to sell a business, business owners would be wise to consider this important fact.

The report sites Neal Isaacs, Owner of VR Business Brokers of the Triangle who states, “Deals are taking longer in due diligence as buyers work hard to validate their investment and make sure that what they’re buying is worth the premium price today’s sellers are commanding.”

So, is now the time to sell? Many experts feel that it is possible to lose a sizable amount of value if one waits too long to sell. Even just a few months can make a huge difference in terms of perceived value and the ultimate sales price. Working with a proven business broker is a key way to ensure that you are selling at the right time and secure the best possible price.

How Customer Concentration Affects Business Valuation

How Customer Concentration Affects Business Valuation

Customer concentration can be an issue when selling your business if any one client accounts for 15% or more of your company’s revenue. It can be a troubling situation to find yourself in because the fewer clients that contribute to your profitability, the greater the chance of losing a sizeable chunk of your income should one or two customers leave.

If this describes your business, you should be taking steps to expand your customer base – especially if you’re thinking of selling. Generally speaking, the less diversified your revenue stream:

- The higher a risk it represents to potential buyers, and

- The lower your business valuation is likely to be

It may still be possible to reap a higher price for your business, however, if you structure its sale to offset buyer risk.

How?

Let’s say one of your customers represents 30% of your revenue. A buyer may be willing to pay one price for the portion of your business that doesn’t rely on that client – 70%, in this case – and do an earnout for the remaining 30%.

In a typical earnout situation, the seller remains involved with their business for an agreed period of time to help keep a lucrative client onboard. If successful, the buyer pays the seller an additional agreed upon amount. If the customer leaves regardless, the seller may forfeit that fee or a portion of the amount.

The downside of an earnout is that it can prevent a quick exit. So if that’s your eventual goal, you should be working to diversify your customer base to strengthen your valuation down the road.

Read More

5 M&A Myths and How to Deal with Them

Where your money is concerned, myths can do damage. A recent Divestopedia article from Tammie Miller entitled, Crazy M&A Myths You Need to Stop Believing Now, Miller explores 5 big M&A myths that can get you in trouble. Miller points out that many of these myths are believed by CEOs, but that they have zero basis in reality.

Myth 1

The first major myth Miller explores is the idea that the “negotiating is over once you sign the LOI.” The letter of intention is, of course, important. However, this is by no means the end of the negotiations and it is potentially dangerous to think otherwise. The negotiations are not concluded until there is a purchasing agreement in place. As Miller points out, there is a great deal that can go wrong during the due diligence process. For this reason, it is important to not see the LOI as the “end of the road.”

Myth 2

Another myth that Miller wants you to be aware of is that you don’t have to take a company’s debt as part of the purchase price. Many business brokers, such as Miller, recommend that buyers don’t take seller paper.

Myth 3

A third myth that Miller explorers is a particularly dangerous one. The idea that everyone who makes an offer has the money to follow through is, unfortunately, simply not true. Oftentimes, people will make offers without securing the money to actually buy the business. No doubt, this wastes everyone’s time. As the business owner, it can derail your progress. If you are not careful, it could actually prevent you from finding a qualified buyer.

Myth 4

Another myth is built around the notion that sellers don’t need a deal team in order to sell their business. Again, this is another myth that has no real foundation in reality. While it may be possible to sell your business without the assistance of an experienced M&A attorney or business broker, the odds are excellent that doing so will come at a price. According to Miller, those working with an investment banker or business broker can expect, on average, 20% more transaction value!

Additionally, there are other dangers in not having a deal team in place. A business broker can handle many of the time-consuming aspects of selling a business, so that you can keep running your business. It is not uncommon for business owners to get stretched too thin while trying to both run and sell a business and this can ultimately harm its value.

Myth 5

Miller’s final myth to consider is that you must sell your entire business. It is true that most buyers will want to buy 100% of a business, but a minority ownership position is still an option. There are many reasons to consider selling a minority stake, so don’t assume that selling your business is an “all or nothing” affair.

Ultimately, Miller lays out an exceptional case for the importance of working with business brokers when selling or buying a business. Business brokers can help you avoid myths. In the end, they know the lay of the land.

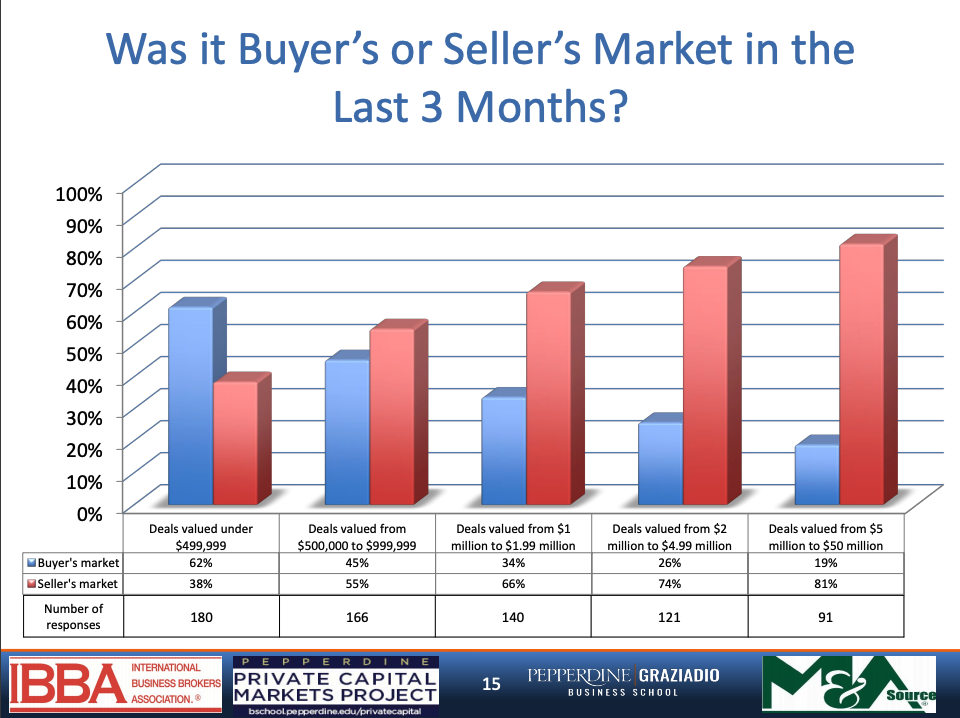

National Survey: Waning Seller’s Market for Sale of Small Businesses Signals a Peak in the Market

Seller’s market sentiment is down in all market segments except for businesses with $5 million to $50 million in enterprise value. Looking back a year, seller’s market sentiment has decreased notably for businesses valued between $1 million – $2 million, dropping six percentage points from Q1 2018 (72%) to Q1 2019 (66%). According to the Q1 2019 Market Pulse Report published by the International Business Brokers Association (IBBA), M&A Source and the Pepperdine Private Capital Market Project seller’s market sentiment increased for businesses valued $5 million to $50 million rising from 77% in Q1 2018 to 81% in Q1 2019.

This is the first time in years that we’ve seen four out of five sectors report a dip in seller market sentiment. This is a sign the market may have peaked and more people are expecting a correction in the year or two ahead. Sellers should consider selling now or waiting another few years before the market will cycle back up to current conditions. To be clear, this doesn’t mean you won’t be able to sell your business over the next few years, but you probably won’t get the multiples you can get today. Any market pessimism or uncertainty will drive down value across the board.

The final sale price of businesses varied depending on its valuation according to the Q1 2019 Market Pulse Report. Lower middle market companies in the $5 million to $50 million range had the highest the final sale price at 101% of the benchmark. On the other hand, small businesses valued under $500,000 had the biggest drop from their asking price with final sale prices going from 91% of the pre-set asking price in Q1 2017 to 85% in Q1 2019.

“Businesses with an enterprise value of $5 million or more are most in demand right now. The market is not cooling at all for those sellers,” said Scott Bushkie, IBBA Marketing Chair and Principal of Cornerstone Business Services Inc. “That’s reflected in supply-demand sentiment and multiples.”

The report also found that the majority of small business owners fail to plan for the sale of their business. Advisors indicated that 90% of business owners with an enterprise value of less than $500,000 conducted no formal planning prior to engagement. Lower middle-market business owners were more proactive, although roughly 48% also failed to make advance plans to sell. Advance planning can help sellers receive the highest market value and decrease the amount of time it takes to sell their business.

About the Market Pulse Report

The Market Pulse Report compares conditions for businesses being sold on Main Street (values of $0 to $2 million) to those being sold in the Lower Middle Market (values of $2 million to $50 million). The Q1 2019 survey was conducted April 11-15, 2019 and was completed by 292 business brokers and M&A advisors. This is the 28th edition of this quarterly report.

About International Business Brokers Association (IBBA) and the M&A Source

Founded in 1983, IBBA is the largest non-profit association specifically formed to meet the needs of people and firms engaged in various aspects of business brokerage and mergers and acquisitions. The IBBA is a trade association of business brokers providing education, conferences, professional designations, and networking opportunities. For more information about IBBA, visit the website at www.ibba.org or follow the IBBA on Facebook, Twitter and LinkedIn.

Founded in 1991, the M&A Source promotes the professional development of merger and acquisition professionals so that they may better serve their clients’ needs and maximize public awareness of professional intermediary services available for middle market merger and acquisition transactions. For more information about the M&A Source visit www.masource.org, or follow the M&A Source on Facebook, LinkedIn, and Twitter.

About Pepperdine University Graziadio Business School

For the last 50 years, the Pepperdine Graziadio Business School has challenged individuals to think boldly and drive meaningful change within their industries and communities. Dedicated to developing Best for the World Leaders, the Graziadio School offers a comprehensive range of MBA, MS, executive, and doctoral degree programs grounded in integrity, innovation, and entrepreneurship. The Graziadio School advances experiential learning through small classes with distinguished faculty that stimulate critical thinking and meaningful connection, inspiring students and working professionals to realize their greatest potential as values-centered leaders. Follow Pepperdine Graziadio on Facebook, Twitter, Instagram, and LinkedIn.

Read More

Whether You Sell Your Business Or Not, The Planning Is The Same

There are many things for you to consider as you think about the future of your business ownership: When is the right time to move on? How much money will I need? How do I even sell this business? These questions dovetail into an important decision you’ll try to make early in the process of planning your future: Whom you’ll sell or transfer your ownership to.

At the end of the day, business owners can sell to two different types of buyers: insiders or outsiders (also referred to as “third parties”). There are different flavors of insiders (e.g., children, key employees, co-owners, and even ESOPs) and third parties (e.g., competitors, venture capitalists, private equity groups, strategic buyers), and owners sometimes get bogged down in what seems like an endless supply of options and strategies to plan for the future of their businesses. However, whether your goal is to sell to an insider or a third party, it’s important to understand that, no matter what, third parties set the standards by which we judge just about all ownership transfers.

It may sound odd that a third party can set the standards of an ownership transfer even if you wanted to transfer your ownership to, say, a family member. But professional buyers, such as private equity groups, set the terms of ownership transfers based on their experience with buying businesses, their competition with other buyers, and their abilities to find strengths and weaknesses in potential acquisitions. In short, they know what makes successful businesses successful, and they demand that the businesses they buy have the elements of a successful business. Like professional buyers, just about anyone else you’ll look to sell to will want those same things.

So, even if your dream is to transfer your ownership to your children or employees, it’s important for you to prepare your business for a third-party sale. Let’s look at three reasons why.

1. Professional buyers determine value.

Professional buyers have the experience, resources, and understanding of the market to find what makes a business successful. They know what a strong management team looks like, they know what good operating systems look like, and they often know how to leverage a business’ strengths beyond what the current owner can do. Thus, they are the arbiters of value.

Because professional buyers can determine a company’s value, it’s wise to build your plans around what professional buyers look for in a potential acquisition. If a professional buyer would value your company highly, it’s likely that other third parties and insiders will do the same. Additionally, if a professional buyer values your company highly, it can mean that your business has elements that make it run smoothly whether you’re present or not.

2. Many buyers want similar elements in their businesses.

Many buyers want strong management teams, a competitive advantage, and a proven growth strategy in place before they buy a business. This is true of professional buyers as well as insiders. Insiders—especially children and co-owners—can develop a blind spot for the company’s weaknesses and take its strengths for granted. This can put you at risk if you’re relying on the company’s performance to provide your income after you exit. On the other hand, if you propose that your top managers take over ownership, they may start to scrutinize flaws in the business, creating skepticism and uncertainty.

You can position yourself to mitigate these risks by planning as though you needed to impress a professional buyer. Again, if a professional buyer sees the value in your business, it’s likely because it has certain elements that allow it to run smoothly, whether you’re in control or not.

3. Third-party sale planning gives you an out.

Sometimes, transfers to insiders can fall apart even with the best planning. For instance, a family member or key employee may decide that the pressures of ownership aren’t worth the benefits and pull out at the last moment. Or, a co-owner you hoped to sell your share of ownership to may realize they aren’t cut out to fill your role. By preparing for a third-party sale even when you don’t intend to sell to a third party, you can give yourself an out if the insider you choose can’t or won’t take the reins.

Many of the big picture elements that go into third-party sale planning apply to planning for an insider transfer. If you’d like to evaluate or begin your plans for the future of your ownership, please contact us today.

Edward W. Cotney

ed@olympustax.com

Olympus Tax, Business and Insurance Solutions, Inc.

4600 Roseville Road, Ste 150 / 260

Sacramento, CA 95660

www.olympustax.com

(530) 913-0562

10 Questions Everyone Should Ask Before Signing on the Dotted Line

Before buying any business, a seller must ask questions, lots of questions. If there is ever a time where one should not be shy, it is when buying a business. In a recent article from Entrepreneur magazine entitled, “10 Questions You Must Ask Before Buying a Business”, author Jan Porter explores 10 of the single most important questions prospective buyers should be asking before signing on the dotted line. She points out to remember that “there are no stupid questions.”

The first question highlighted in this article is “What are your biggest challenges right now?” The fact is this is one of the single most prudent questions one could ask. If you want to reduce potential surprises, then ask this question.

“What would you have done differently?” is another question that can lead to great insights. Every business owner should be an expert regarding his or her own business. It only makes sense to tap into that expertise when one has the opportunity. The answers to this question may also illuminate areas of potential growth.

How a seller arrives at his or her asking price can reveal a great deal. Having to defend and outline why a business is worth a given price is a great way to determine whether or not the asking price is fair. In other words, a seller should be able to clearly defend the financials.

Porter’s fourth question is, “If you can’t sell, what will you do instead?” The answer to this question can give you insight into just how much bargaining power you may have.

A business’ financials couldn’t be any more important and will play a key role during due diligence. The question, “How will you document the financials of the business?” is key and should be asked and answered very early in the process. A clear paper trail is essential.

Buying a business isn’t all about the business or its owner. At first glance, this may sound like a strange statement, but the simple fact is that a business has to be a good fit for its buyer. That is why, Porter’s recommended question, “What skills or qualities do I need to run this business effectively?” couldn’t be any more important. A prospective buyer must be a good fit for a business or otherwise failure could result.

Now, here is a big question: “Do you have any past, pending or potential lawsuits?” Knowing whether or not you could be buying future headaches is clearly of enormous importance.

Porter believes that other key questions include: “How well documented are the procedures of the business?” and “How much does your business depend on a key customer or vendor?” as well as “What will employees do after the sale?”

When it comes to buying a business, questions are your friend. The more questions you ask, the more information you’ll have. The author quotes an experienced business owner who noted, “The more questions you ask, the less risk there will be.”

Business brokers are experts at knowing what kinds of questions to ask and when to ask them. This will help you obtain the right information so that you can ultimately make the best possible decision.

A Step by Step Overview of the First Time Buyer Process

A recent article on Businessbroker.net entitled, First Time Buyer Processes by business broker Pat Jones explores the process of buying a business in a precise step-by-step fashion. Jones notes that there are many reasons that people buy businesses including the desire to be one’s own boss. However, he is also quick to point out that buyers should refrain from buying a business that they simply don’t like. In the quest for profits, many prospective owners may opt to do this, but it could ultimately lead to failure.

Step One – Information Gathering

For Jones, there are seven steps in the business buying process. At the top of the list is to gather information on businesses so that one has an idea of what kind of businesses are appealing.

Step Two – Your Broker

The second key step is to begin working with a business broker. This point makes tremendous sense; after all, those new to the business buying process will benefit greatly from working with a guide with so much experience. Business brokers can gain access to information that prospective business owners simply cannot.

Step Three – Confidentiality and Questions

The third step in the process is to sign a confidentiality agreement so that you can learn more about a business that you find interesting. Once you have the businesses marketing package, you’ll want to have your broker schedule an appointment with the seller. It is vitally important that you prepare a list of questions on a range of topics. There is much more to buying a business than the final price tag. By asking the right questions, you’ll be able to learn more about the business and its long-term potential.

Step Four – Evaluation

In the fourth step of the business buying process, you’ll want to evaluate all the information that you have received from the seller. Once again, a business broker can be simply invaluable, thanks to years of hands-on experience, he or she will know how to evaluate a seller’s information.

Step Five – The Decision

In the fifth step, you’ll need to decide whether or not you are making an offer. If you are making an offer, you will, of course, want it to be written and include contingencies.

If your offer is accepted, then the process of due diligence begins. During due diligence, you and your business broker will look at everything from financial statements to tax returns. You will evaluate the company’s assets. Again business brokers are experts at the due diligence process.

Buying a business is an enormous commitment. Making certain that you’ve selected the right business for you is one of the most critical decisions of your life. Having as much competent and experienced help as possible is of paramount importance.