BizBuySell’s Annual Insight Report- 2019 Small Business Market: Uncertainty Creates Opportunity and Risk

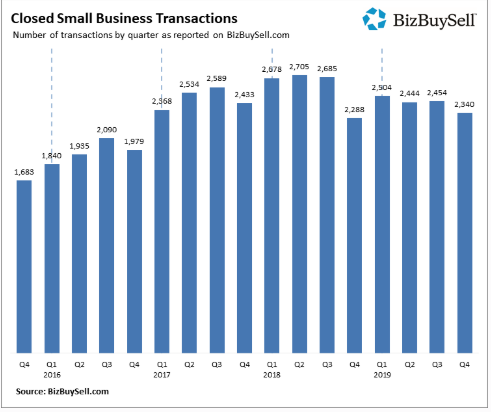

BizBuySell’s Annual Insight Report shows that while small business sales still remain at historically high levels, 2019 transactions took a five percent dip from record-setting 2018 levels. The number of small businesses that changed hands in 2019 dropped slightly compared to last year according to the latest BizBuySell Insight Report, a nationally-recognized economic indicator that aggregates statistics from business-for-sale transactions reported by participating business brokers nationwide. The Insights Report also touches on several compelling demographic trends, including the Baby Boomer’s growing likelihood of selling their businesses as they age and seek retirement, as well as the causes of current market conditions.

In total, 9,746 closed sales were reported by brokers in 2019, a 5.5 percent decrease from the 10,312 deals reported in 2018, which set the BizBuySell record for most transactions. While full-year activity slowed compared to 2018, 4th quarter transactions bounced back to positive growth and it’s important to remember that levels remain historically high.

Still, there are many issues surrounding the market that could cause hesitation when considering a sale, particularly for owners who are having to juggle the dynamic of running a business at the same time of managing through policy changes. In fact, business owner confidence dropped 6 points in 2019 according to BizBuySell’s Annual Confidence Index, largely due to political and economic uncertainty.

Click here for the full report.

Read More

The Top Ways to Create an Attention-Grabbing Sales Ad to Sell Your Business

A major part of selling your business is getting the word out. After all, the more people that know your business is for sale, the better off you’ll be. In Bob House’s recent article, “How to Create an Effective Business for Sale Ad and Ensure It Gets the Best Result,” House gives readers an assortment of tips that he believes will help sellers attract higher offers from real buyers.

Getting the Word Out

As House wisely points out, many sellers wait until the last second to dive in and create a good sales ad. In fact, many sellers fail to grasp the real importance of creating a quality and compelling advertisement. Imagine creating a good sales ad like you would going fishing with a group of friends. The more friends you have on your fishing trip, the greater the odds that someone catches a fish. In much the same way, the more people who know you are selling your business, the greater the chances that you’ll get some serious “bites.”

Tips for Receiving More Attention

House has five key tips for attracting more attention from prospective buyers via your sales ad. At the top of the list is to be descriptive. Your sales ad should give an excellent description of your business and its unique features. As House notes, you want to “paint a clear picture.” In other words, now is not the time for mystery. You want prospective buyers to have a very clear idea of what kind of business they could possibly buy.

Headlines Count

Secondly, you should have a great headline. People have always skimmed, but the rise of the Internet has taken skimming to a whole new level. Your sales ad should have a very engaging and interesting headline. You want to capture people’s attention. A good place to start is by determining what your business’s best feature is and emphasizing that feature in your headline.

Incorporate Top-Notch Images

Third, the old saying that a picture is worth a thousand words absolutely applies to selling a business. Just as a great headline will capture people’s attention, the same holds true for a great picture. Consider having a professional photographer take the photo, as he or she may have tips to make your business look its best that you may simply not know.

Your Financials

Fourth, your ad should definitely include key financials. Any serious buyer will be very concerned, if not obsessed, with your financials. Information such as cash flow and income statements are a good idea as may potential buyers focus their business searches around key financial metrics.

Don’t Forget the Final Step

Finally, if there has ever been a time in your life to proofread, this is the time. In fact, you should consider hiring a proofreader to look over your ad for grammar and spelling mistakes. As House notes, you want prospective buyers to realize that you are attention oriented and responsible. A simple grammar or spelling mistake could wreck a potential deal.

Creating a great sales ad is an art form. One of the best ways to ensure that you have a great sales ad is to work with an experienced business broker. Business brokers know what buyers are looking for, have great marketing professionals at their disposal, and can help you frame your business in the best light possible.

What Do You Need to Do to Get Your Business Ready to Sell?

In his recent article in Smart Business entitled, “How to get your business, and yourself, ready for sale,” author Adam Burroughs explores the key points of getting your business ready to sell. Burroughs points to the truism that, at some point, almost every business owner must sell his or her business. For this reason, it is critical to think about what it takes to get your business ready to sell. Simply stated, it is best to explore and plan for selling your business long before you actually need to place your business on the market. Let’s explore some key points for selling your business.

Broadening Your Options

Burroughs interviews Scott McRill at Clark Schaefer Hackett. McRill notes, “The sooner you think about your exit, the more options you’ll have for yourself and the business when the time comes.” A savvy business owner will always want to give himself or herself as many options as possible. McRill wisely points out that early planning is key, and a failure to engage in early planning could lead to a lower selling price. If you want to get the best price for your business, then planning for the eventual sale as far in advance as possible is a good move.

Planning in Advance

According to Burroughs, business owners should start planning to sell their business at least 2 to 3 years before they actually plan to sell. Part of the reason for this is so that business owners will have enough time to make operational improvements designed to maximize the business’s overall value.

A Financial Review

At the top of every business owners “preparing to sell” list is to have a third-party review the business’s financial situation. This is excellent advice for, as frequent readers of this blog know, any serious prospective buyer will look long and hard at your business’s financials. Getting your business’s financial house in order means that you should turn to an accounting firm for help. You’ll want to review financial statements for at least the previous 2 to 3 years.

Burroughs points out that when it comes to selling a business, there are many variables that business owners often overlook. At the top of the list is the management team.

Your Management Team

Prospective buyers can get very nervous about the stability of the management team once ownership has changed hands. Often, the new buyer may only sign on the dotted line if the owner agrees to stay on after the sale during a transition period. Having a competent and proven team in place, one that is dedicated to staying with the company will help you get your business ready to sell.

There are a lot of variables involved in preparing to sell a business. The sooner that you get experts involved in the process, the better off you will be. A business broker can serve as a guide – one that can point you in the right direction. Find a broker with an abundance of experience, and you’ll have an invaluable ally who can help you navigate the process. It can take a lot of time and effort to sell a business. Working with a business broker can keep you from reinventing the wheel at every step of the process.

Selling Your Business, Taxes & Tax Structures

It is never too early to start thinking about what tax structure you should use when it comes time to sell your business. A simple, but undeniable, rule of life is that taxes matter and they can’t be overlooked. Author Tim Fries at The Tokenist has written an excellent and quite detailed overview article on what tax issues business owners need to consider before selling their business. His article, “What Tax Structure Should You Use When Selling Your Business?” explores many aspects of a topic that many business owners fail to invest enough time in, namely taxes.

As Fries astutely points out, the taxes involving the sale of a business can be complex and are usually unknown to those selling a business for the first time. Your tax structure can influence how much money you receive at the closing of your deal, so it’s a very good idea to pay attention to all aspects of taxation and your business. It is key to remember, “When you are selling your business – as far as taxes are concerned – you’re ultimately selling a collection of assets.”

Fries points out that taxes and selling a business are no small matter. It is possible that up to 50% of the sale of a business can go to taxes. Don’t worry if you are learning this for the first time and feel more than a little shocked. However, this fact does a good job of illuminating the importance of setting up the right tax structure for your business. While you might not be able to get around taxes altogether by investing the time and effort to set up the right structure for your business, you can keep from paying more taxes than is necessary.

There are a lot of variables that go into how much you will ultimately have to pay in taxes. Let’s take a look at some of the key questions Fries raises in his article.

- Is your sale considered ordinary income or is the sale considered capital gains?

- Are you operating as an LLC, a sole proprietorship, a partnership or are you operating as a corporation?

- What portion of the sale price goes to tangible assets as compared to intangible assets?

- Is there a difference between your tax basis and the proceeds from your sale?

- What does your depreciation look like?

- Don’t expect that the buyer will instantly agree to your terms.

- Realize that the decisions you make during negotiations with a buyer will have tax implications.

- Is an installment sale right for your business?

- With C corporations, sellers usually want a stock sale whereas buyers generally prefer an asset sale.

- Cashing out immediately, where you receive all your funds at once, will increase your tax liability.

- Have you considered switching to an S corporation?

- Have you consulted with experts to decide which tax structure is best for you?

- Have you consulted with a business broker?

Selling a business is obviously complicated. Finding a seasoned business broker can help you demystify many aspects of buying and selling a business. Ultimately, having the best deal structure and finding the right buyer can be a labyrinthian process. Having the very best professional help in your corner is simply a must.