IBBA 2018 Q3 Market Pulse Report- Why Are Business Owners Selling?

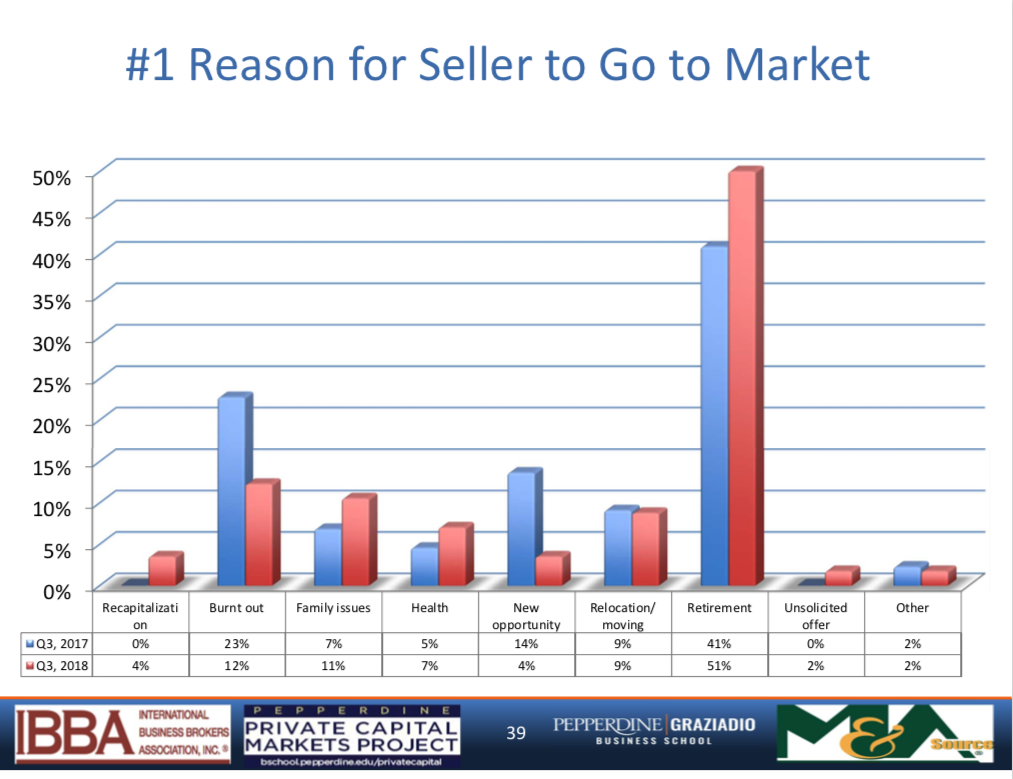

The recent Q3 2018 Market Pulse Survey Report indicates that retirement continues to lead as the number one reason for selling a company (52% for companies valued at $1M-$2M, and 56% for those valued at $2M-$5M).

Because a business often represents up to 70% percent of the owner’s overall wealth, it is critical that they take a proactive approach when preparing for their exit. Owners who succeed in harvesting years of hard work will not only financially benefit them on a personal level, but they will have more wealth to pass on to their families.

Earlier this year, the Market Pulse Survey Report indicated that business owners who sold their business for $2M to $5M preplanned at twice the rate of business owners selling in the $1M to $2M range. Proactive planning is important and the better prepared an owner is, the better results they will experience. Yet studies show that 60% of business owners who did not preplan were unable to sell their business for their expected value, bringing truth to the adage those who fail to plan, plan to fail.

To start planning, determine how much money you will need to receive for your business to be able to live the life you want afterward. Think about these questions: What do I have now, and what do I need? Most people do not have their “number” figured out, but with a little work, you can get there quickly. Get some professional help from a wealth manager or financial planner to fine-tune that number.

We are here to help when you need to determine the marketability and approximate value of your business. For more information, please contact our office at 916-993-5433 or email at randy@evobizsale.com.

Read More

Day One is the Day to Prepare Your Exit

Pepperjam CTO, Greg Shepard recently published “Planning Your Exit Should Begin When You Launch” in Entrepreneur magazine. In this article, Shepard puts forward a variety of thought-provoking ideas including that entrepreneurs should be thinking about partnering early on with those they believe will ultimately want to buy their business.

Thinking Ahead

Much of Shepard’s thinking centers around the fact that a large percentage of startups end in acquisitions. In particular, he notes that in 2017, “mergers and acquisitions accounted for 93 percent of the 809 ventures capital-backed exits, yielding a total of $45.6 billion in disclosed exit value.” Not too surprising, he also points out that according to a recent Silicon Valley Bank survey, over 50% of all startups are “hoping for an acquisition.”

For this reason, Shepard points out that entrepreneurs should be thinking about who may potentially acquire them from day one. In particular, startups will want to build their companies in such a way that they will be attractive for acquisition at a later date.

Making one’s startup attractive for acquisition means thinking about such details as the Ideal Customer Profile, Ideal Employee Profile, and Ideal Buyer Profile. This will help startups build the most attractive acquisition friendly company possible. According to Crunchbase, exit opportunities frequently present themselves well before a company’s Series B funding.

Building Successful Strategies

Startups simply must understand who their customer is and why their particular product is attractive to that customer. Likewise, having the right kind of employees with the right kind of training and know how is key. Hiring the best talent is definitely a way for a startup to make itself more attractive for a potential future acquisition.

Shepard believes that once you understand your customer and have the right team to support your vision, you’ll want to focus in on companies that are most likely to be interested and construct an “optimal buyer pool.” Finding this optimal buyer pool means finding businesses that serve similar markets and then making sure that your product, as well as your business model, both address an overlooked need within the existing customer base. Combine all of these variables together, and your company will be more attractive for an acquisition.

Let Innovation Drive You

Another key point in Shepard’s article is that startups will want to provide products or services that potential buyers are currently not providing to their customers. Additionally, he states that “Disruptors should seek out companies that are truly driven by innovation-perhaps those that have already established or partnered with innovative labs or accelerators.”

Ultimately, it is critical for startups to understand where they could fit within a larger organization. Understanding this will help entrepreneurs make their company more acquisition friendly.

What Makes the Sale of a Business Fall Through?

There are a myriad of reasons why the sale of a business doesn’t close successfully; these multiple causes can, however, be broken down into four categories: those caused by the seller, those caused by the buyer, those that just happen (“acts of fate”), and those caused by third parties. The following examines the part each of these components can play in contributing to the wrecked deal:

The Seller

1. In some instances, the seller doesn’t have a valid reason for entering into the sale process. Without a strong reason for selling, he or she has neither the willingness to negotiate nor the flexibility to see the sale to a conclusion. Without such a commitment, the desire to sell is not powerful enough to overcome the many complexities necessary to finalize the sales process.

2. Some sellers are merely testing the waters. As detailed above, they are not at that “hungry” stage that provides the push toward a successful transaction. These sellers merely want to see if anyone wants to buy their business at the price they would like to receive.

3. Many sellers are unrealistic about the price they want for their business. They may be sincere about wanting to sell, but they are unable to be realistic about how the marketplace will value the business. The demand for their business may not be there.

4. Some sellers fail to be honest about their business or its situation. They may be hiding the fact that new competition is entering the market, that the business has serious problems or some other reason the business is not salable under existing circumstances. Even worse, some sellers do not disclose that there is more than one owner and that they are not all in agreement about selling the business.

5. A seller may decide to wait until a buyer is found and then check with their outside advisors about the tax and/or legal consequences. At this point, the terms of the deal have to be altered, and the buyer won’t agree. Sellers should deal with these complications ahead of time. Nobody likes changes–especially buyers!

The Buyer

1. The buyer may not have an urgent need or a strong desire to go into business. In many cases the buyer may begin with positive intentions, but then doesn’t have the courage to make “the leap of faith” necessary to go through with the sale.

2 Some buyers, like sellers, have very unrealistic expectations regarding the price of businesses. They are also uneducated about the nature of small business in general.

3. Many buyers are not willing to put in the hours or do the type of work necessary to operate a business successfully.

4. Buyers can be influenced by others who are opposed to the purchase of a business. Many people don’t or can’t understand the need to be “your own boss.”

Acts of Fate

These are the situations that “just happen,” causing deals to fall through. Even considering the strong hand of fate, many of these situations could have been prevented.

1. A buyer’s investigation reveals some unmentioned or unknown problem, such as an environmental situation. Or, perhaps there are financial deficiencies discovered by the buyer. Unfortunately, these should have been on the table from the beginning of the selling process.

2. The seller may not be able to substantiate, at least to the buyer’s satisfaction, the earnings of the business.

3. Problems may arise, unknown to both the seller and the buyer, with federal, state, or local governmental agencies.

Third Parties

1. Landlords may become difficult about transferring the lease or granting a new one.

2. Buyers and/or sellers may receive overly-aggressive advice from outside advisors, usually attorneys. Attorneys, in their zeal to represent their clients, forget that the goal is to put the deal together. In some cases, they erect so many roadblocks that the deal can only fall apart.

Most of the problems outlined here could have been resolved before the selling process was too far advanced. There are also some problems that could not have been avoided–people do sometimes enter situations with the best of intentions only to find out that this is not the right answer for them after all. These are the exceptions, however. Most business sales can have happy endings if potential difficulties are handled at the appropriate time.

Business brokers are aware of the various ways a deal may fall through. They are experienced in resolving issues before the business goes onto the market or before a buyer is introduced to the business. To buy or sell a business successfully, sellers should resolve any potential deal-wreckers, following the advice of a professional business broker.

Although business brokers cannot provide legal advice, they are familiar with the intricacies of the business sale. They are also familiar with local attorneys who specialize in the details of these transactions. These attorneys will usually be more efficient, and therefore more cost-effective, than the attorney who handles a general practice.

When It’s Time To Sell Your Business, Put Your Strengths First

Putting your strengths first will help you sell your business. While this may seem obvious, a surprising number of business owners will either improperly index the strengths of their business or fail to emphasize those strengths adequately. In this article, we will examine five key business strengths that you should focus on when it comes time to sell.

Understand Your Buyer

You know your business, but you don’t necessarily know what buyer is best for it in the long run. If you’ve never sold a business before (and most business owners haven’t), then you may not know how to best position and present your business for sale.

A business broker is immensely valuable in this regard. These professionals are very good at determining which prospective buyers are serious and which ones are not. Additionally, a business broker will use their own databases of prospective and vetted buyers and try to match your business up with the prospective buyers that are most likely to be a good fit. When dealing with a buyer, a seasoned business broker will put emphasis on your strengths whenever possible.

Be Sure to Maintain Normal Operations

Selling a business can be very demanding and underscores, once again, the value of working with a business broker. A business broker will focus on selling your business so that you have more time to focus on the day-to-day of running your business.

The last thing you want is to waste your time on buyers who are not serious. Remember, if your business suffers as a result of the time you spend away from your business in the sale process, then the value of your business to prospective buyers could suffer.

Determining the Best Price

If you incorrectly price your business, you could dramatically reduce the interest. Business brokers are experts at pricing businesses and can help you determine the best possible price. Many business owners have unrealistic valuations and others may even undervalue their businesses or they fail to incorporate all aspects of their business. Working with a professional business broker can help you quickly achieve the best price. The best price possible will work to maximize the strengths of your business.

Getting Your Business Ready for Sale

There is a lot that goes into getting your business ready to sell. The simple fact is that getting your business ready to sell isn’t a one-dimensional process, but instead involves every aspect of your business. Getting your business ready to sell isn’t about making it look presentable and putting a “new coat of paint” on things, although this is a factor.

Instead it is necessary to have every aspect of your business in order. From paperwork such as tax returns, contracts and forms to a business plan and more, it is important to consider every aspect of your business. You should consider what you would want to see if you were the one looking to buy the business. Be sure to do everything possible to build up your strengths.

Confidentiality

If word gets out that your business is up for sale, there could be a range of problems. Employees, including key management, could begin looking for other jobs and suppliers and key buyers could begin to look elsewhere. In short, a breach of confidentiality could lead to chaos.

Getting your business ready for sale means factoring in the strengths and weakness of your business then fixing weaknesses whenever possible and building upon your strengths. Working with a business broker can help you address every point covered in this article and more.

Copyright: Business Brokerage Press, Inc.

Read More